Health Insurance is No Longer True Insurance

The most common question we receive at AFLDS is: “How do I find a Frontline Doctor who will put my best interest first and will take my insurance?”

The uncomfortable truth is that it has become extremely difficult — nearly impossible — for physicians to consistently prioritize patients when they are deeply entangled in today’s insurance system. The incentives are stacked against ethical, patient-centered care.

This is the first in a series of issues briefs examining how tax policy and government intervention fundamentally broke American healthcare — and the doctor-patient relationship.

The American promise is rooted in the right to life, liberty, and the pursuit of happiness — rights that are impossible without private property and control over your own earnings.

When government tax policy and corporate interests seize effective control over how you spend your money on healthcare — one of the largest expenses in most people’s lives — they turn free citizens into financial dependents. This is government-enabled corporate theft of your income, your choices, and your autonomy.

It has slowly moved America toward a socialist model where third parties decide what care you receive and how much of your own money you are allowed to keep.

Financial slaves are not free.

Until we understand how this happened, we cannot reclaim our liberty or fix the broken system.

The Core Problem

True insurance exists to solve a specific economic problem: pooling risk for rare, unpredictable, and financially devastating events. A house fire, fatal car accident, or major medical catastrophe can wipe out a family financially. Many pay modest premiums so the few who suffer catastrophe are protected.

American health insurance has abandoned this model. It has become a comprehensive prepayment system for routine, predictable expenses — physicals, prescriptions, office visits, and everyday care. When expected consumption is routed through insurance, it stops being risk pooling. It becomes prepaid spending buried under layers of billing, coding, prior authorizations, networks, and bureaucracy.

This is not insurance. It is a structural distortion that drives up costs, obscures prices, weakens competition, removes patients from economic decision-making, and transforms physicians into participants in a reimbursement system rather than independent professionals serving patients directly.

The Original Purpose of Insurance

Insurance is expensive because preparedness is expensive. Insurers must maintain reserves, staff, and infrastructure ready for large claims at any moment. People accept this cost for true financial protection.

For most forms of insurance—auto, home, and life—the distinction between catastrophic financial loss and routine spending remains intact. Health insurance in the United States gradually moved in a different direction.

Using insurance for routine care is like using an emergency room for a sore throat. You don’t just pay for the visit — you pay for the entire trauma-ready system. When predictable expenses go through insurance, administrative friction explodes while real risk protection shrinks. Patients lose price visibility. Competition weakens. The person receiving care is no longer the true customer.

How the Mistake Happened: The Tax Policy Pivot

The pivotal shift began during World War II. In 1943, the IRS ruled that employer-paid health insurance premiums would not be treated as taxable income to employees, while individually purchased insurance remained taxable. Congress made this permanent in 1954 under Internal Revenue Code §106.

This created a powerful tax asymmetry. In a 35% tax bracket, a $10,000 employer-provided policy effectively costs the employee far less than buying the same policy independently (roughly one-third cheaper, and even more when including payroll taxes). Employers, competing for workers under wage controls, began offering broader and broader benefits. The larger the policy, the greater the tax advantage.

Over decades, routine medical services migrated into insurance plans. Federal policies reinforced this employer-based model:

- ERISA (1974): Promoted prepaid, managed care and gatekeeping.

- The HMO Act (1973): Strengthened employer control.

- DRGs (1983): Expanded complex coding systems.

- Managed Care Expansion (1980s–90s): Added prior authorization and restricted networks.

- The Affordable Care Act (2010): Expanded coverage but preserved the employer-based system with more mandates.

What began as catastrophic protection became a third-party payment machine for everyday care.

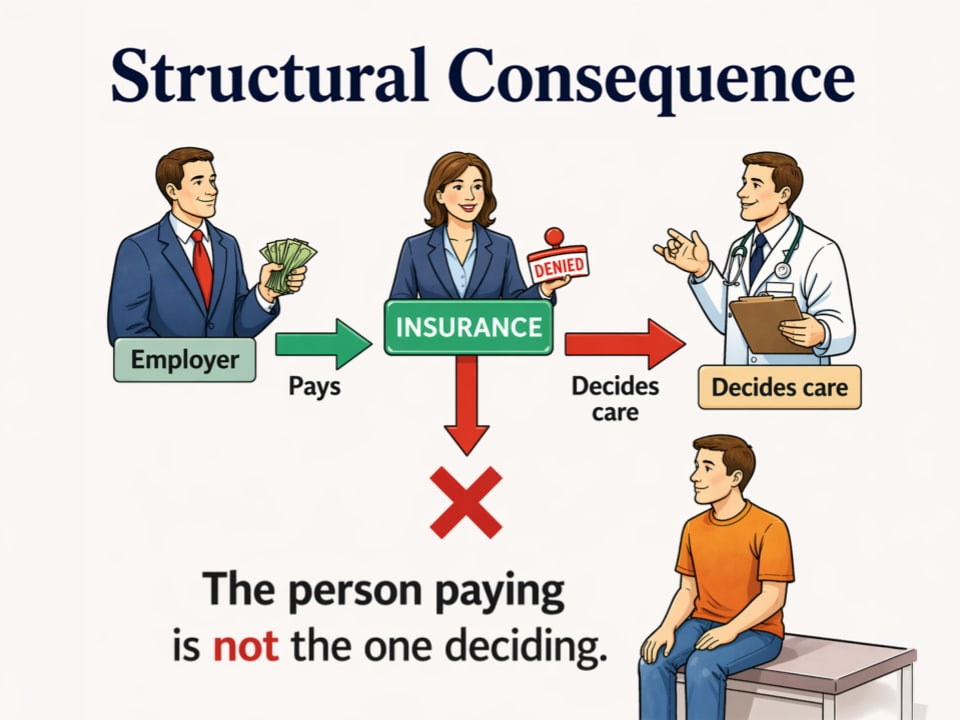

Incentive Inversion: Who Pays vs. Who Decides

Today, most working Americans get insurance through their job. But you ultimately pay for it through lower wages. Yet you don’t choose the plan, negotiate the price, or control the benefits. Employers and insurers decide.

This is incentive inversion: The person paying (you) is not the person deciding. Patients become passive recipients while physicians operate within networks, prior authorization requirements, and reimbursement formulas. Prices become opaque and competition shifts from serving patients to satisfying employer contracts and regulatory compliance.

The result is a system organized around institutional negotiation rather than direct consumer choice, with administrative costs now consuming roughly 30% of U.S. healthcare spending — far higher than peer nations.

Real-World Consequences

- For Patients: High premiums plus large out-of-pocket costs (deductibles, copays, coinsurance) that can still reach tens of thousands of dollars. Limited doctor choice of doctor. A system feels designed for everyone except you.

- For Physicians: Shift from independent professionals to “providers” burdened by paperwork, prior authorizations, and coding requirements. Clinical judgment is filtered through institutional protocols. Many experienced doctors burn out and leave practice early.

- For the System: Persistent inflation, massive price dispersion for identical services, overutilization, and misallocated resources. The U.S. spends nearly one-fifth of GDP on healthcare—roughly double most advanced economies—yet achieves worse outcomes in many areas.

Separating Fact From Narrative

This system is not the natural result of free markets or medical complexity. It is the direct, predictable outcome of tax policy that heavily favors employer-mediated, third-party payment. Economists have warned about these distortions for decades.

Your frustration with high costs, surprise bills, and limited choices is completely rational. The great mistake was policy-driven, not the result of greed or market failure alone.

Bottom Line

Health insurance stopped functioning as true insurance when it began covering routine, predictable expenses. The result is a distorted system of opacity, administrative bloat, lost patient control, and relentless cost inflation.

But how did we get so deeply trapped in this system — and what specific mechanisms keep honest doctors from practicing freely?

The next brief will examine the hidden architecture that makes real patient-centered medicine so difficult inside today’s insurance model.